- Original Medicare and Medicare Advantage: The Core Differences Explained

- Medicare Advantage vs. Original Medicare Costs: What the Numbers Mean

- How Your Medicare Plan Choice Directly Affects Medication Adherence

- What the Medicare Decision Means for Residents in Long-Term Care

- How DosePacker Supports Medication Adherence Across Both Plan Types

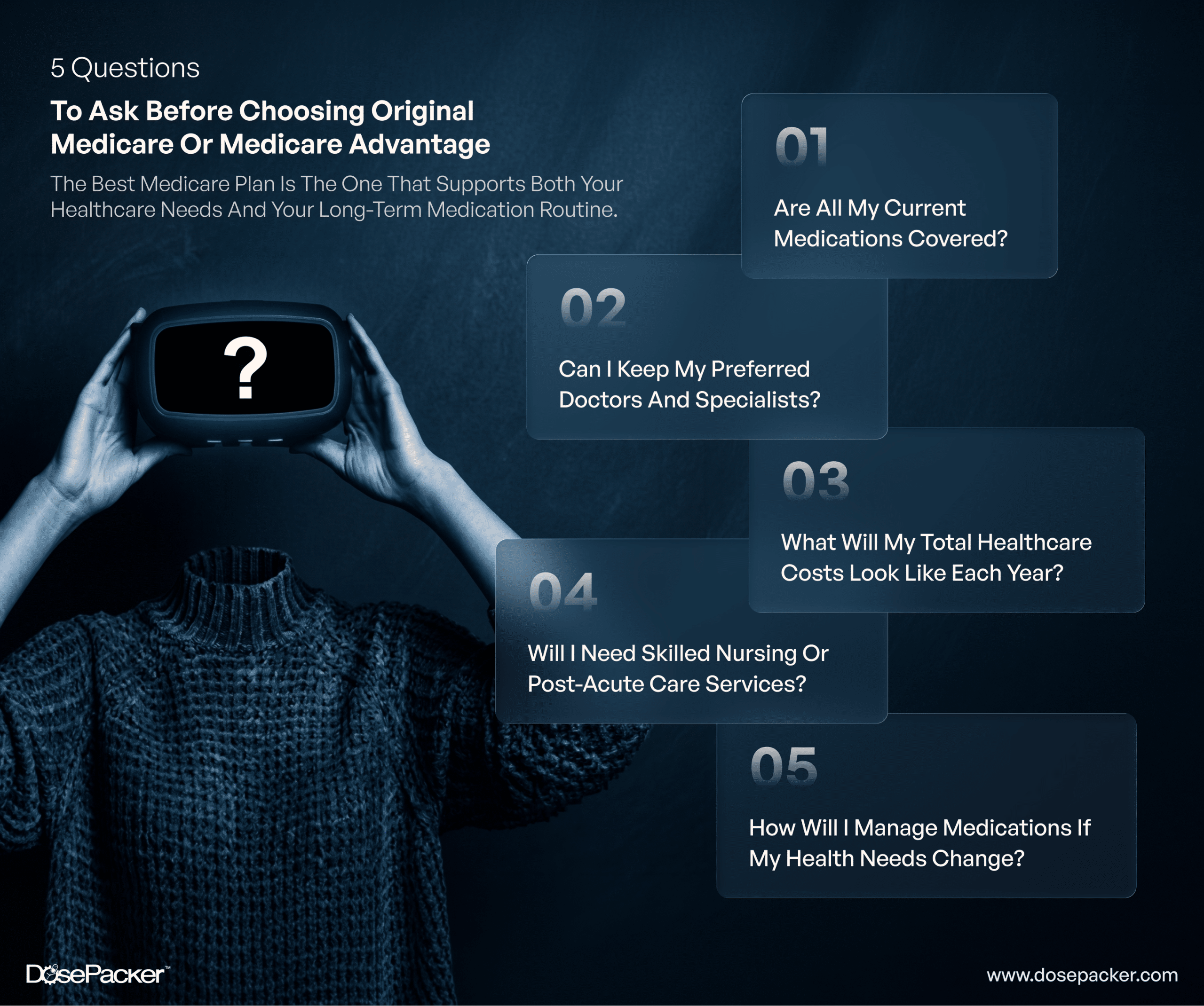

- Original Medicare vs. Medicare Advantage: Making the Right Choice for Your Healthcare Needs

- FAQs

Unlock the latest in medication management technology and grow your care community with us.

Every year, millions of Americans approaching 65 face the same decision: enroll in original Medicare or choose a Medicare Advantage plan. It sounds straightforward, but the stakes are far higher than the paperwork suggests.

According to the CDC, 95% of adults age 60 and older have at least one chronic condition, and nearly 80% have two or more. For this population, the difference between original Medicare and Medicare Advantage goes beyond premiums. It shapes which medications get covered, which pharmacies you can use, and whether the plan you choose will support your medication adherence over the long term. The wrong decision can lead to coverage gaps, escalating out-of-pocket costs, and care disruptions that compound over time.

At DosePacker, we work directly with long-term care communities and the residents and families they serve. We see every day how insurance plan design affects real medication routines, and how the right support structure can protect adherence regardless of which plan a patient carries. This guide is built on that experience. It covers what each plan offers, where costs diverge, and how to think through the decision in a way that protects both your health and your financial stability.

Comparing Plans? Don’t Overlook Medication Adherence!

Original Medicare and Medicare Advantage: The Core Differences Explained

Before comparing original Medicare or Medicare Advantage, it helps to understand what each one is fundamentally designed to do.

Original Medicare is a federal program administered directly by the Centers for Medicare and Medicaid Services. Part A covers inpatient hospital care, and Part B covers outpatient services, physician visits, and preventive care. Beneficiaries can see any provider nationwide who accepts Medicare, which offers broad flexibility.

However, original Medicare does not include prescription drug coverage by default. For medications, beneficiaries must enroll separately in a Part D plan. Coverage for dental, vision, and hearing requires supplemental (Medigap) insurance purchased separately.

Medicare Advantage, also known as Part C, is a private insurance alternative that bundles Part A and Part B benefits into a single plan. Most Medicare Advantage plans include Part D prescription drug coverage, and many offer extras like dental, vision, and fitness benefits. In exchange, beneficiaries generally must use a network of approved providers and may need referrals to access specialist care.

This structural difference between original Medicare and Medicare Advantage is the foundation. The complexity deepens when you examine costs and continuity of care in real-world settings.

Medicare Advantage vs. Original Medicare Costs: What the Numbers Mean

Cost is almost always the first factor people weigh when comparing Medicare Advantage and original Medicare. But the answer depends heavily on how much care you use, not just what you pay each month.

Premiums, Deductibles, and Out-of-Pocket Exposure

With original Medicare, most beneficiaries pay no Part A premium if they or their spouse paid Medicare taxes for at least ten years. The Part B standard premium is set annually by CMS. The critical vulnerability with original Medicare alone is that there is no annual cap on out-of-pocket spending. A hospitalization, an extended course of outpatient treatment, or a serious illness can create costs that accumulate quickly. Many beneficiaries address this by pairing original Medicare with a Medigap policy, which adds a monthly premium but limits financial exposure.

Medicare Advantage vs. original Medicare costs look attractive on paper for many enrollees. Numerous plans carry low or even zero monthly premiums. But these plans come with network restrictions, prior authorization requirements, and cost-sharing structures that can make them more expensive in practice when care needs increase. The annual out-of-pocket maximum is genuine protection, but reaching it requires consistently navigating the plan’s rules.

There is no universally cheaper option between the two. The right comparison is the total expected cost given your specific health profile, not just the premium line.

Which Medicare Plan Covers Prescription Drugs

This question is among the most consequential for anyone managing a chronic condition. Original Medicare does not cover prescription drugs without a standalone Part D plan. Most Medicare Advantage plans include drug coverage as part of the package, which is one of the most cited reasons beneficiaries choose it.

But integrated drug coverage is only as valuable as the formulary behind it. A medication that is fully covered under one Medicare Advantage plan may sit on a high cost-sharing tier under another. Before enrolling in any plan, verify that every medication in your current regimen is covered at a cost-sharing level that is sustainable month to month. This step is one many beneficiaries skip, and it is frequently where coverage surprises emerge mid-year.

How Your Medicare Plan Choice Directly Affects Medication Adherence

The link between insurance plan design and medication adherence is well-documented. When cost-sharing is too high or formulary uncertainty casts doubt on whether a medication will remain affordable, patients skip doses, split pills, or discontinue treatment. For older adults managing diabetes, hypertension, or heart disease, that kind of disruption has direct clinical consequences.

This is where a comprehensive medication review becomes essential, regardless of which plan a beneficiary selects. A CMR is a structured consultation, typically conducted by a pharmacist, that evaluates whether your current medications are clinically appropriate, whether interactions or duplications exist, and whether your insurance plan is genuinely supporting your regimen. Under original Medicare with Part D and under most Medicare Advantage plans, eligible beneficiaries can request a CMR at no additional cost.

DosePacker’s pharmacy teams conduct these reviews regularly for the residents and patients we serve. A comprehensive medication review is a practical checkpoint that ensures the plan a beneficiary chooses on paper is actually delivering what they need at the point of care.

What the Medicare Decision Means for Residents in Long-Term Care

For individuals in skilled nursing facilities, assisted living communities, or receiving post-acute care and SNF services, the original Medicare vs. Medicare Advantage decision carries layers of complexity that go beyond what most enrollment guides address.

Original Medicare covers a defined period of skilled nursing care following a qualifying hospital stay. Coverage rules are standardized and apply uniformly regardless of which facility a beneficiary uses, as long as the facility accepts Medicare. Medicare Advantage plans must offer equivalent SNF benefits by law, but network requirements and prior authorization processes vary significantly by plan. Some plans require beneficiaries to use only in-network facilities, which can limit options in certain regions and create complications when a resident needs to transfer for specialized care.

Families making coverage decisions for loved ones in these settings should consult with their facility’s LTC Pharmacy Services team before enrolling or switching plans. A pharmacist who manages medications in that setting has direct, practical experience with how specific plans affect coverage timelines, formulary access, and medication adherence for that population. That on-the-ground perspective is one of the most underutilized resources available to families navigating this decision.

DosePacker’s LTC Pharmacy Services team works alongside care communities to identify coverage gaps before they affect residents and to ensure that transitions between plans, care levels, or facilities do not interrupt medication continuity.

How DosePacker Supports Medication Adherence Across Both Plan Types

Whether a patient is enrolled in original Medicare or a Medicare Advantage plan, the downstream challenge remains the same: ensuring medications are taken correctly, consistently, and without interruption. Plan selection determines what is covered. What happens after that depends on the tools and systems in place to support adherence at the point of care.

DosePacker’s integrated ecosystem addresses this directly. The DosePack Compliance Pack organizes medications into clearly labeled, unit-dose packaging, reducing the confusion that can lead to missed or doubled doses. For residents and families managing complex medication regimens in care settings, the packaging itself becomes a daily, visible reinforcement of the prescribed routine.

The DoseMinder smart medication management device extends that support further, delivering real-time reminders and tracking whether doses have been taken. For older adults in assisted living or independent living settings, DoseMinder closes the gap between a prescription being filled and a medication actually being taken on schedule, a gap that insurance plans alone cannot address.

The MyDoses App brings caregivers and family members into that visibility, flagging missed doses before they become clinical problems and giving families peace of mind when they cannot be physically present.

Across all of these tools, DosePacker’s medication adherence solutions are designed to function within the realities of whichever Medicare plan a patient carries.

Original Medicare vs. Medicare Advantage: Making the Right Choice for Your Healthcare Needs

There is no one-size-fits-all answer in the original Medicare vs. Medicare Advantage debate. The right choice depends on your healthcare needs, prescription medications, provider preferences, financial situation, and whether you anticipate requiring long-term or post-acute care services. Understanding the difference between original Medicare and Medicare Advantage can help you avoid unexpected costs, coverage limitations, and disruptions to care. Most importantly, whichever option you choose should support consistent access to medications, healthcare providers, and the resources needed to maintain long-term health and medication adherence.

Support Better Medication Outcomes Beyond Your Medicare Plan

DosePacker’s integrated ecosystem helps support medication adherence, simplify administration, and improve visibility across the entire medication journey.

FAQs

Original Medicare is a federal program offering broad provider access and standardized coverage. Medicare Advantage is a private insurance alternative that bundles benefits, typically including drug coverage, within a defined network. The core tradeoff is flexibility versus consolidation.

Original Medicare does not cover prescriptions without a standalone Part D plan. Most Medicare Advantage plans include drug coverage, but formularies vary. Always verify your specific medications are covered before enrolling.

Medicare Advantage plans are required to cover SNF stays at least as generously as original Medicare, but network restrictions and prior authorization rules apply. For beneficiaries in post-acute care and SNF settings, it is important to confirm which facilities are in-network before a care transition.

Facebook

Facebook

WhatsApp

WhatsApp

Instagram

Instagram

Twitter

Twitter

Gmail

Gmail

LinkedIn

LinkedIn